What Are Leveraged & Inverse ETFs?

6/23/2026

Leveraged and inverse ETFs promise 2x or 3x the daily move of an index, and funds like TQQQ and SQQQ can hand a trader a year's worth of gains in a week. The catch is a quiet force called volatility decay that can bleed them dry even when you are right about direction.

What Are Leveraged and Inverse ETFs?

A leveraged ETF is an exchange-traded fund that uses financial derivatives to deliver a multiple of an index's daily return. A leveraged and inverse ETF family covers both directions: leveraged funds amplify the move in the same direction (a "bull" fund), while inverse funds move opposite to the index (a "bear" or "short" fund). The most common multiples are 2x and 3x, and the inverse versions are written as -1x, -2x, or -3x.

The word that matters most in any prospectus is daily. These funds are engineered to hit their target multiple over a single trading session, not over a week, a month, or a year. ProShares launched the first US leveraged ETFs in 2006, Direxion followed with 3x funds in 2008, and the flagship ProShares UltraPro QQQ (TQQQ) and its inverse twin SQQQ arrived in February 2010. Today the category spans indexes, sectors, bonds, commodities, and even single stocks.

Leveraged ETFs (bull funds)

A 3x leveraged ETF like TQQQ aims to return +3% on a day the Nasdaq-100 (QQQ) rises 1%, and -3% on a day it falls 1%. Other examples include Direxion Daily Semiconductor Bull 3x (SOXL) and ProShares UltraPro S&P 500 (UPRO). These are pure directional bets with the volume turned up.

Inverse ETFs (bear or short funds)

An inverse ETF profits when its index falls. SQQQ targets -3x the daily move of the Nasdaq-100, so a 1% Nasdaq drop is designed to lift SQQQ about 3%. The single-leverage ProShares Short S&P 500 (SH) simply moves opposite the index at -1x. Inverse funds let an investor express a bearish view or hedge a portfolio without a margin account and without unlimited short-selling risk, because the most you can lose is what you put in.

How Do Leveraged ETFs Actually Work?

A leveraged ETF cannot magically multiply returns out of thin air. It borrows exposure. To deliver 3x the daily move with only the cash investors deposit, the fund holds a mix of index securities plus total return swaps and index futures that provide the extra notional exposure. If the fund has $1 billion in assets, it must maintain roughly $3 billion of index exposure.

The role of swaps and futures

Most of the leverage comes from swap agreements with investment banks: the fund agrees to pay a financing rate and receives the index's return (or its inverse) in exchange. These derivatives are cheap to scale but carry financing costs that rise with interest rates, which is one reason leveraged ETFs are more expensive to run than a plain index fund.

Why they rebalance every single day

To keep the leverage ratio pinned at 3x, the fund must rebalance at the close of every trading day. The mechanics are brutally simple and work against you in chop:

- After an up day, the fund's exposure has grown beyond 3x, so it must buy more exposure to reset, effectively buying high.

- After a down day, its exposure has shrunk below 3x, so it must sell exposure to reset, effectively selling low.

This forced "buy high, sell low" rhythm is the engine behind volatility decay. It is not a bug in any one fund. It is baked into the daily-reset design of the entire leveraged and inverse ETF category.

What Is Volatility Decay?

Volatility decay (also called beta slippage or volatility drag) is the gradual loss of value in a leveraged or inverse ETF caused by daily compounding in a choppy market. The painful part: a leveraged fund can lose money even when the underlying index ends flat. The more the index zigzags, the more the fund bleeds.

The compounding math

A useful approximation for a leveraged fund's expected return is:

Here L is the leverage factor and sigma is the index's daily volatility. The second term is the decay. For a 3x fund with 2% daily volatility, the daily drag is roughly:

That 0.12% a day compounds. Notice the L(L-1) term: it equals 2 for a 2x fund and 6 for a 3x fund, so a 3x ETF suffers three times the decay of a 2x ETF, not 1.5 times. Leverage punishes volatility geometrically.

A worked example you can check

Imagine an index that rises 10% one day and falls 10% the next. Common sense says it should be roughly flat. Watch what leverage does:

| Fund | Day 1 (+10% index) | Day 2 (-10% index) | Ending value | Total return |

|---|---|---|---|---|

| Index (1x) | 100 → 110 | 110 → 99 | 99 | -1.0% |

| 2x leveraged | 100 → 120 | 120 → 96 | 96 | -4.0% |

| 3x leveraged | 100 → 130 | 130 → 91 | 91 | -9.0% |

The index lost 1%. The 2x fund lost 4%, and the 3x fund lost 9%, all from a single round trip. Stretch that over a quarter of sideways volatility and a 3x fund can underperform by double digits while the index goes nowhere.

Leveraged ETFs vs the Index: A Multi-Day Example

Decay is not destiny. Leveraged ETFs do not always lose to their target multiple. The outcome depends entirely on the path the index takes, not just the destination.

| One-month market path | Index return | "Ideal" 3x | Actual 3x fund (typical) |

|---|---|---|---|

| Smooth, low-volatility uptrend | +15% | +45% | Often greater than +45% (compounding helps) |

| Flat but choppy (round trips) | 0% | 0% | Negative (decay bleeds it) |

| Smooth, low-volatility downtrend | -15% | -45% | Often worse than -45% for a bull fund |

The takeaway: leveraged ETFs reward strong, persistent trends with low day-to-day noise and punish whipsaw. A smooth grind higher can actually beat the naive 3x multiple because gains compound on gains. A volatile market that ends in the same place still drains the fund. That is exactly why these are trading tools, not buy-and-hold building blocks. For a calmer way to compound, compare it with the discipline of dollar-cost averaging versus lump-sum investing.

How Do Inverse ETFs Work for Hedging?

Inverse ETFs shine as short-term hedges. Suppose you own a basket of tech stocks and want protection into a risky catalyst, like a Federal Reserve meeting or a big earnings night, without selling your winners and triggering taxes. Buying a slug of SQQQ offsets some of the downside: if the Nasdaq drops 3% that day, a -3x fund is built to rise about 9%, cushioning the hit.

The advantages over traditional shorting are concrete:

- No margin account required and no borrow fees to locate shares.

- Losses are capped at your investment, unlike a naked short where losses are theoretically unlimited.

- One-click access in any standard brokerage account.

But the same daily-reset decay applies. An inverse ETF is a tactical, days-long hedge, not insurance you can buy and forget. If you hold SQQQ for a month while the market grinds higher, decay plus the upward drift will gut the position. To think through when a hedge is even worth putting on, gauge the mood with the live Fear and Greed reading below and read more in our guide on how to hedge your portfolio against risk.

Popular Leveraged and Inverse ETFs in 2026

Most leveraged and inverse ETFs track broad indexes or hot sectors. Here are the heavyweights traders watch, with their objectives and approximate expense ratios. Always confirm the current fee on the issuer's page, since ratios change with fee waivers.

| Ticker | Objective | Daily target | Underlying | Provider | Approx. expense ratio |

|---|---|---|---|---|---|

| TQQQ | Bull | +3x | Nasdaq-100 | ProShares | ~0.82% |

| SQQQ | Inverse | -3x | Nasdaq-100 | ProShares | ~0.95% |

| SOXL | Bull | +3x | Semiconductors | Direxion | ~0.75% |

| SOXS | Inverse | -3x | Semiconductors | Direxion | ~0.94% |

| UPRO | Bull | +3x | S&P 500 | ProShares | ~0.91% |

| SPXU | Inverse | -3x | S&P 500 | ProShares | ~0.90% |

| SH | Inverse | -1x | S&P 500 | ProShares | ~0.88% |

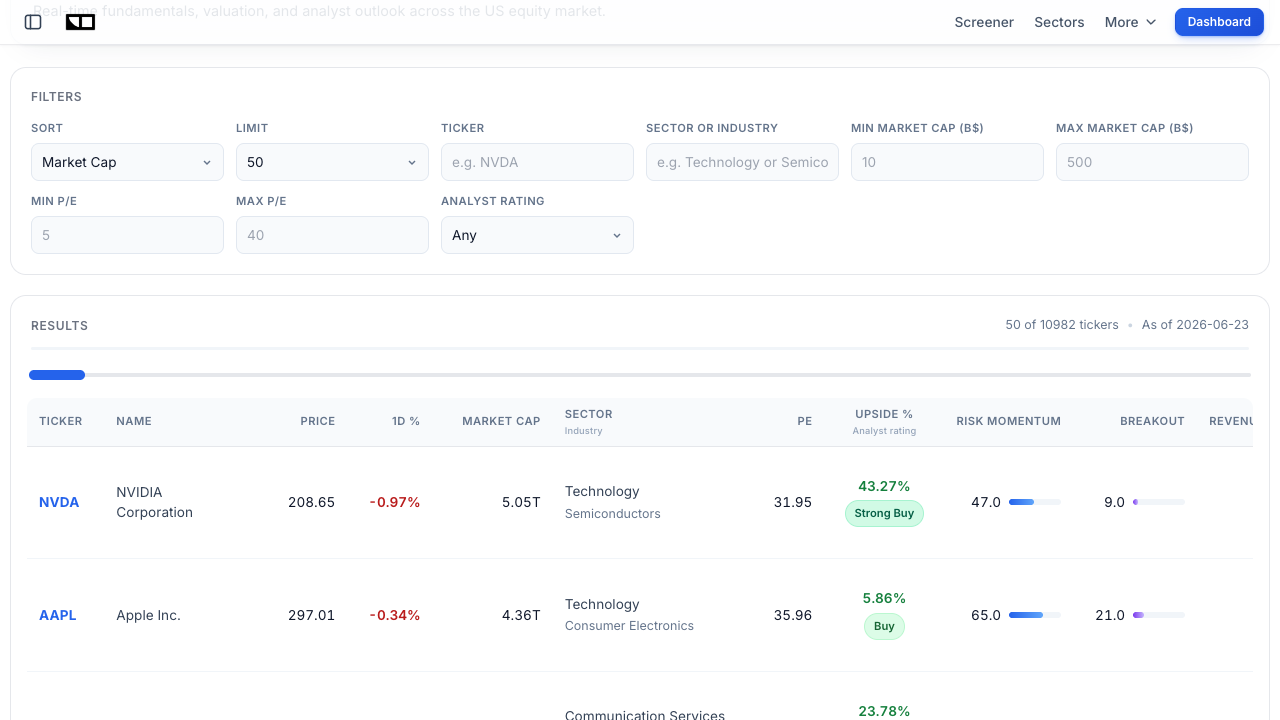

Two things jump out. First, the fees are steep: 0.75% to 0.95% versus roughly 0.03% to 0.20% for a plain S&P 500 or Nasdaq index fund. Over a year that gap is a meaningful headwind on top of decay. Second, the most popular funds cluster around the most volatile corners of the market, especially semiconductors, which is precisely where decay does the most damage. Before you trade any underlying, it pays to screen the actual companies driving the index. You can filter by sector, valuation, and momentum on the Finance Halo market screener.

Real-World Example: The June 2026 Chip Selloff

Late June 2026 offered a live lesson. On June 23, a rotation out of artificial-intelligence and semiconductor stocks slammed the tape: the Nasdaq Composite fell about 2.4%, Micron (MU) cratered 11.4%, NVIDIA (NVDA) slid 3.2%, and Western Digital dropped 8.4%. For anyone holding the inverse 3x semiconductor fund SOXS, that was a banner day, with the fund designed to climb roughly three times the chip index's percentage drop.

Here is the trap, though. A trader who bought SOXS or SQQQ in early June and held through the chop did not simply collect "3x the decline." The market did not fall in a straight line. It rallied on some days, dumped on others, and the daily resets ate into the position the whole way. The investor who nailed the direction over the month could still have ended with a fraction of the naive 3x payoff because of the path. Timing the entry and exit within days, not weeks, was the difference between a profit and a slow bleed. For the broader context of that drawdown, see our breakdown of whether the AI trade is cracking and the difference between a correction and a bear market.

Are Leveraged ETFs Good for Long-Term Investing?

For the vast majority of investors, the honest answer is no. Regulators have said so explicitly. FINRA's Regulatory Notice 09-31 (June 2009) warns that daily-reset leveraged and inverse ETFs "typically are unsuitable for retail investors who plan to hold them for longer than one trading session, particularly in volatile markets." The SEC's investor bulletin echoes that these are "highly complex" products meant to be held for a single day.

That said, there is a vocal community that has held 3x funds like TQQQ for years and done extraordinarily well, because US large-cap tech spent much of the last decade in a powerful low-volatility uptrend, the ideal regime for leverage. The problem is survivorship bias. The same fund can fall 80% to 95% in a bear market and take years to recover, if it recovers at all, because climbing back from a 90% loss requires a 900% gain. Risk-adjusted, the ride is far rougher than the headline returns suggest, which is why metrics like the Sharpe ratio matter so much when you add leverage.

- If you must hold long term, understand you are making a concentrated bet that volatility stays low and the trend stays up. Size it as the speculative sliver of a portfolio, not the core.

- A diversified core belongs in low-cost index funds. See our comparison of MSCI World versus the S&P 500 for sensible building blocks.

Common Mistakes to Avoid

- Treating them like regular ETFs: Buying TQQQ for your retirement account and forgetting it ignores daily resets and decay. Fix: use them only for defined, short-horizon trades.

- Ignoring volatility decay: Assuming "the Nasdaq is up 20% this year, so TQQQ must be up 60%" is wrong if the path was choppy. Fix: judge performance against the fund's actual chart, not a multiplied index.

- Oversizing the position: Putting 25% of your portfolio in a 3x fund is really a 75% directional bet. Fix: size the leverage, not the dollars, so total exposure stays sane.

- Holding an inverse hedge too long: Keeping SQQQ on for weeks while the market drifts up guarantees death by decay. Fix: set a time stop and a price stop when you open the hedge.

- Averaging down into a losing leveraged position: Adding to a falling 3x fund compounds both the loss and the decay. Fix: cut losers fast; leverage magnifies mistakes.

- Overlooking the expense ratio: A 0.95% fee plus financing costs is a constant headwind. Fix: factor total cost into any multi-day hold and prefer the cheapest fund for the same exposure.

How to Use Leveraged and Inverse ETFs Responsibly

If you decide these tools fit your trading, a few rules keep them from blowing up your account. Leverage rewards discipline and destroys improvisation.

- Define the trade before you enter. Write down the catalyst, the time horizon (ideally hours to a few days), the price target, and the exit. If you cannot name all four, do not put it on.

- Use hard stop-losses. A 3x fund can move 10% to 20% in a session. Set stops based on the underlying's volatility. Our guide to the Average True Range (ATR) shows how to size stops to real volatility instead of guessing.

- Keep position sizes tiny. Many disciplined traders cap any single leveraged position at 1% to 5% of the portfolio so a worst-case gap cannot do permanent damage.

- Confirm the trend and the noise. Leverage loves smooth trends and hates chop. Check market breadth and sentiment on the Finance Halo market intelligence dashboard before committing.

- Research the underlying, not just the wrapper. A 3x semiconductor fund is only as good as the chips inside it. Vet those names on the stock screener first.

Frequently Asked Questions

What is the difference between a leveraged ETF and an inverse ETF?

A leveraged ETF amplifies an index's daily move in the same direction (for example, +3x). An inverse ETF moves opposite the index (for example, -3x), rising when the index falls. Some funds, like SQQQ, are both leveraged and inverse, targeting -3x the daily return.

Can you lose all your money in a leveraged ETF?

You can lose most of it, but not more than you invest, which is one advantage over shorting on margin. A 3x fund would need its index to fall about 33% in a single day to go near zero, and providers can reverse-split or restructure failing funds. Over time, volatility decay can quietly erase the bulk of a position even without a crash.

Why does my leveraged ETF lose money when the index is flat?

Because of volatility decay. Daily rebalancing forces the fund to buy after up days and sell after down days. In a choppy market that round-trips to the same level, this "buy high, sell low" cycle compounds losses, so the fund can finish lower even though the index is unchanged.

How long should you hold a leveraged or inverse ETF?

Regulators and the funds themselves intend them to be held for a single trading day or, at most, a few days while a clear trend is in force. The longer the hold and the more volatile the market, the further your return drifts from the stated multiple.

Are leveraged ETFs good for hedging a portfolio?

Inverse ETFs can be effective short-term hedges because they require no margin account and cap your loss at the amount invested. They are poor long-term insurance, however, since decay erodes them if you hold through sideways or rising markets.

What is the expense ratio on leveraged ETFs?

Typically 0.75% to 0.95% per year, far above the roughly 0.03% to 0.20% of a standard index ETF. For example, TQQQ runs around 0.82% net and SOXL around 0.75%. Financing costs on the swaps add an additional, less visible drag.

What happens to leveraged ETFs in a market crash?

A 3x bull fund can fall 80% to 95% in a sustained bear market and may take years to recover, since recovering from a 90% loss needs a 900% gain. A 3x inverse fund can surge during the crash, but only if you time the entry and exit within the move rather than holding through the recovery.

Conclusion

Leveraged and inverse ETFs are some of the most powerful and most misunderstood tools in the market. Used as designed, for short, high-conviction trades with tight risk control, they let you express a strong view or hedge a portfolio without margin. Used carelessly, as set-and-forget holdings, volatility decay, daily resets, and fat expense ratios can grind a position to dust even when your market call is correct.

Remember the three things that matter most: these funds target a daily multiple, decay punishes volatility geometrically (a 3x fund bleeds three times faster than a 2x fund in chop), and regulators consider them unsuitable for long-term holding. Keep positions small, use stops, and treat any leveraged ETF as a scalpel, not a foundation. Build the core of your portfolio with low-cost, diversified funds and reserve leverage for the speculative edges.

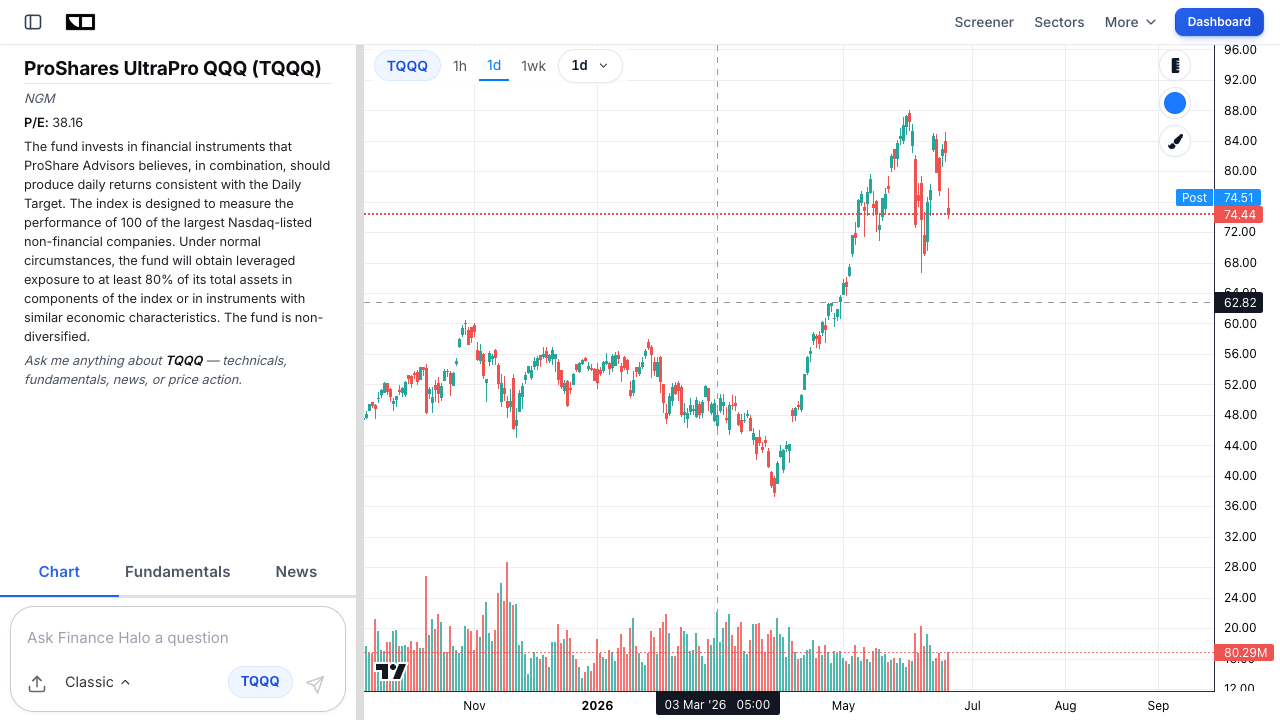

Try it yourself: Analyze TQQQ with Finance Halo's AI assistant to get instant technical analysis, price action, and risk insights on any leveraged or inverse ETF in seconds.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Leveraged and inverse ETFs carry substantial risk and are not suitable for all investors. Always do your own research before making investment decisions.