What Is EBITDA? A Beginner's Guide

6/18/2026

EBITDA is one of the most quoted - and most abused - numbers in all of investing. This beginner's guide explains exactly what EBITDA is, how to calculate it in two minutes, why Wall Street loves it, and why Warren Buffett and Charlie Munger think you should treat it with deep suspicion.

What Does EBITDA Stand For?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a measure of a company's operating profitability that deliberately ignores four things: how the business is financed (interest), where it is taxed (taxes), and two non-cash accounting charges that spread the cost of long-lived assets over time (depreciation and amortization).

The idea is to get as close as possible to the cash-generating power of the core business before financing and accounting decisions muddy the picture. Two companies in the same industry can report wildly different net income simply because one carries a lot of debt and the other does not, or because one operates in a high-tax country. EBITDA tries to put them on a level playing field so you can compare apples to apples.

Here is what each letter actually removes:

- Interest: the cost of debt. A company with a large loan pays interest; a debt-free competitor does not. Removing interest isolates operations from the balance sheet.

- Taxes: corporate income tax, which varies by jurisdiction and changes with tax law. Stripping it out improves cross-border comparability.

- Depreciation: the gradual expensing of physical assets like factories, machines, and servers over their useful life.

- Amortization: the same idea applied to intangible assets like patents, software, and acquired goodwill.

EBITDA first became popular in the 1980s during the leveraged-buyout boom, when private-equity buyers needed a quick way to gauge whether a target generated enough cash to service the mountain of debt they planned to load onto it. That origin story matters: EBITDA was born as a debt-coverage proxy, not as a measure of true shareholder profit. We will come back to that distinction.

The EBITDA Formula: Two Ways to Calculate It

There are two standard ways to calculate EBITDA, and both should land on the same number. Which one you use depends on which line of the income statement you start from.

Method 1: The bottom-up approach (from net income)

Start at the very bottom of the income statement and add back everything EBITDA excludes:

This version makes the acronym literal: you are taking earnings and adding back the four items in the name. It is the most common textbook formula.

Method 2: The top-down approach (from operating income)

If you start from operating income, also called EBIT (Earnings Before Interest and Taxes), interest and taxes are already excluded, so you only add back the two non-cash charges:

This is usually faster because operating income is reported directly on the income statement, and depreciation and amortization are listed on the cash flow statement (in the operating-activities section). According to Corporate Finance Institute, both routes are valid; analysts simply pick whichever inputs are easiest to find.

| Approach | Starting Point | What You Add Back |

|---|---|---|

| Bottom-up | Net income | Interest + Taxes + Depreciation + Amortization |

| Top-down | Operating income (EBIT) | Depreciation + Amortization |

A quick note on where to find the inputs: net income and operating income live on the income statement, while depreciation and amortization are most reliably pulled from the cash flow statement. You can find all of these in a company's quarterly (10-Q) and annual (10-K) filings on the SEC EDGAR database. Learning to read these statements is the foundation of fundamental analysis - our guide on how to analyze a stock before buying walks through the process step by step.

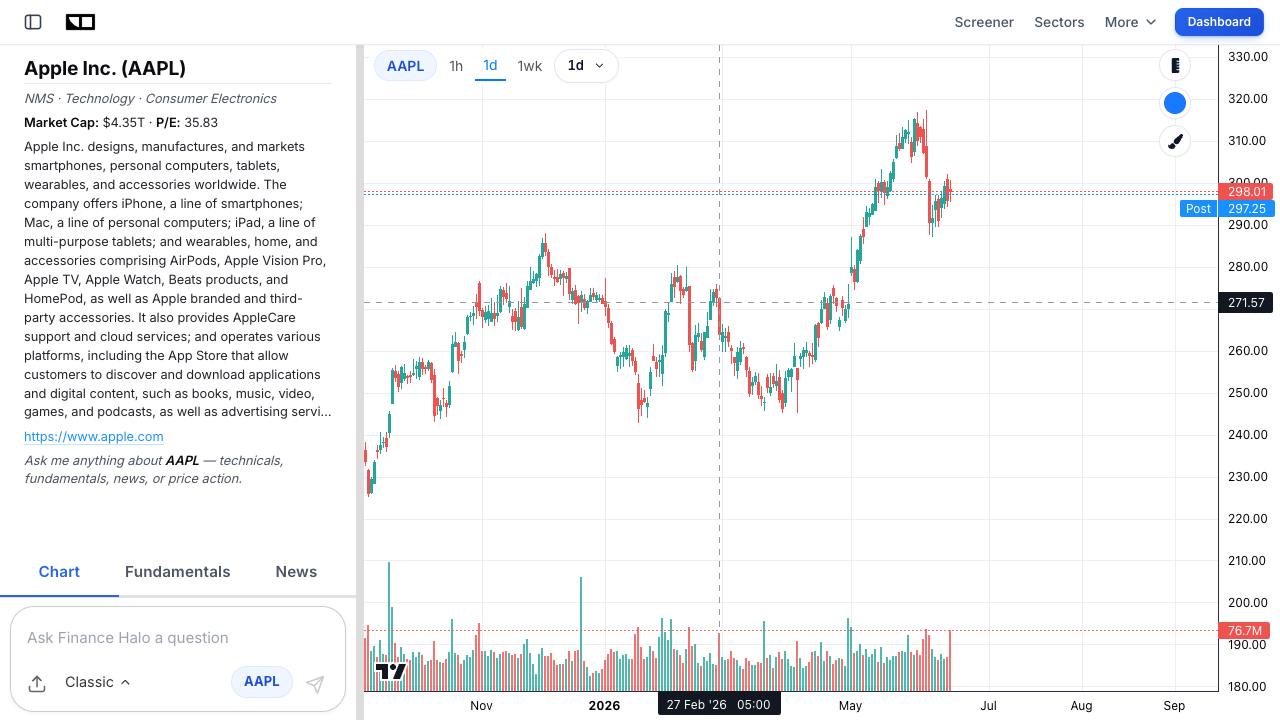

Worked Example: How to Calculate Apple's EBITDA

Theory is easy; let us run real numbers. We will use Apple (AAPL) and its fiscal 2025 results, which the company reported in its official financial statements.

For fiscal year 2025, Apple reported:

- Total revenue: $416.2 billion

- Operating income (EBIT): $133.1 billion

- Depreciation and amortization: roughly $11.7 billion

Using the top-down method:

So Apple generated roughly $144 billion in EBITDA in fiscal 2025. That is an enormous figure, and it tells you the core business throws off cash at extraordinary scale. Notice how small depreciation and amortization are relative to operating income - that is typical of an asset-light, brand-driven business. For a capital-intensive company like an airline or a telecom, the D&A add-back would be a much larger slice of EBITDA, which is exactly where the metric starts to mislead (more on that below).

What Is EBITDA Margin and What Is a Good One?

EBITDA margin expresses EBITDA as a percentage of revenue. It answers a simple question: of every dollar of sales, how much survives as core operating profit before financing, tax, and non-cash charges?

Back to Apple: $144.8 billion of EBITDA on $416.2 billion of revenue is an EBITDA margin of about 34.8%. That is elite. For context, a small business with $1.5 million in revenue and $227,000 in EBITDA would have a 15% margin - perfectly respectable, but a different universe from Apple's.

As a rule of thumb, an EBITDA margin above 10% is viewed positively by most analysts. Here is a rough framework, though the "good" number always depends on the industry:

| EBITDA Margin | Interpretation | Typical Examples |

|---|---|---|

| Below 10% | Thin - low pricing power or a cost-heavy model | Grocers, airlines, distributors |

| 10% - 20% | Healthy and average | Industrials, retailers, autos |

| 20% - 40% | Strong operating efficiency | Consumer brands, pharma, hardware |

| Above 40% | Exceptional - high pricing power | Software, luxury, semiconductors |

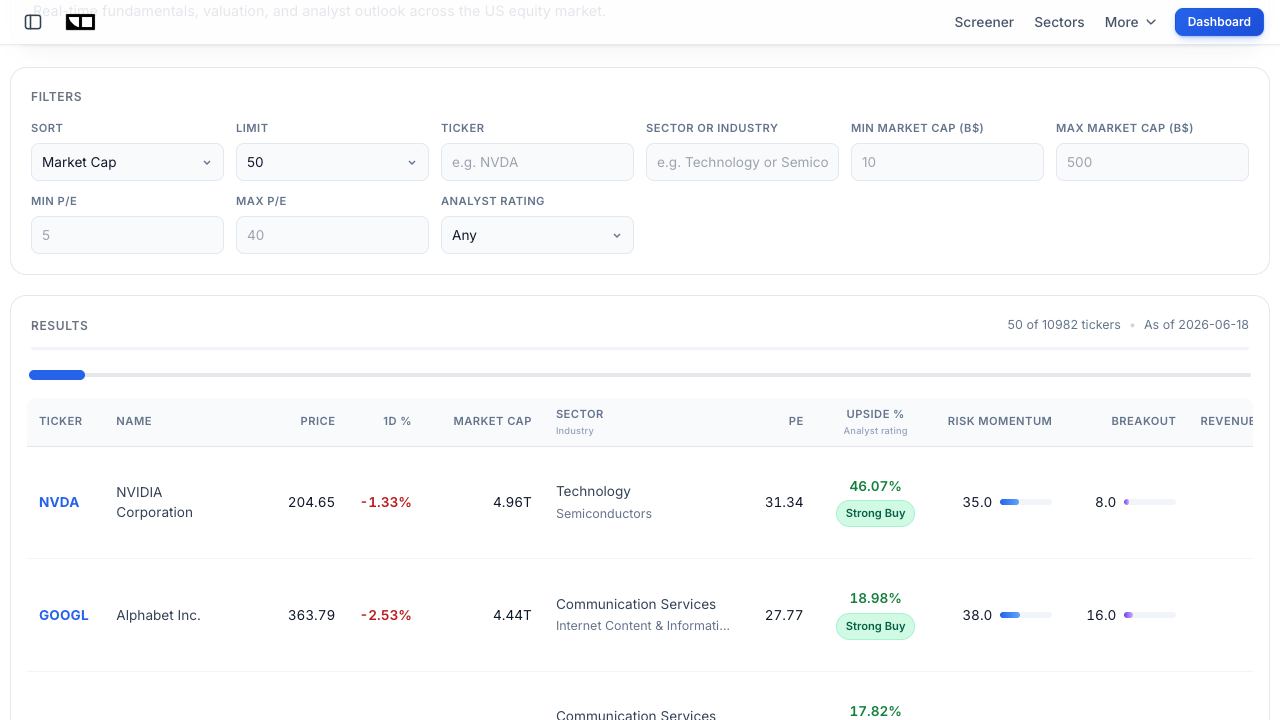

The higher the margin, the smaller a company's operating expenses are relative to its revenue. But never compare margins across unrelated industries. A 12% margin is excellent for a supermarket and alarming for a software company. Compare a company only to its direct peers, which is exactly what a tool like the Finance Halo screener is built for.

Why Do Investors Use EBITDA?

If Buffett dislikes it so much, why is EBITDA on practically every analyst report and acquisition memo? Because, used carefully, it has genuine strengths:

- Comparability across capital structures. By removing interest, EBITDA lets you compare a debt-heavy firm with a debt-free one on operating performance alone.

- Comparability across tax regimes. Removing taxes helps when comparing a US company to one based in Ireland or Singapore.

- It smooths out lumpy accounting. Depreciation schedules are partly a choice. Two identical factories can be depreciated over different timelines, distorting net income. EBITDA sidesteps that.

- It is a fast proxy for cash generation. For a stable, asset-light business, EBITDA is a reasonable first approximation of operating cash flow.

- It is the basis for valuation multiples. EV/EBITDA is the dominant multiple in mergers, acquisitions, and private equity.

EBITDA is a starting point for analysis, not a verdict. It pairs naturally with other valuation tools. If you want the full toolkit, see our breakdown of the P/E ratio vs EPS vs PEG and our guide to what counts as a good P/E ratio.

EBITDA vs. Net Income vs. Free Cash Flow

This is the section that separates beginners from informed investors. EBITDA, net income, and free cash flow all claim to measure "profit," but they measure very different things. Confusing them is how investors get burned.

| Metric | What It Captures | What It Ignores | Best Used For |

|---|---|---|---|

| EBITDA | Core operating profit before financing and non-cash charges | Interest, taxes, capital spending, working capital | Comparing operations across companies |

| Net Income | The bottom-line accounting profit shareholders keep | Non-cash distortions; capital spending timing | EPS, P/E ratio, GAAP reporting |

| Free Cash Flow | Actual cash left after running and reinvesting in the business | Nothing major - it is the most complete cash measure | Judging true value creation and dividends |

The single most important blind spot in EBITDA is capital expenditures (capex). EBITDA adds back depreciation as if it were free money, but depreciation is the accounting echo of cash the company already spent (or will spend again) on equipment. A telecom that must constantly rebuild its network, or an airline that must buy new planes, can post a healthy EBITDA while generating little or no free cash flow because every dollar gets plowed back into capex just to stand still.

Free cash flow is the honest scorecard. The gap between EBITDA and free cash flow tells you how capital-hungry a business really is. When that gap is wide and persistent, EBITDA is flattering the picture. Net income sits in the middle: it captures depreciation and interest (which EBITDA ignores) but can still be distorted by one-time accounting items.

What Is EV/EBITDA? The Valuation Multiple

EBITDA's most popular use is not as a standalone number but as the denominator in a valuation multiple: EV/EBITDA, or enterprise value divided by EBITDA. It is the EBITDA world's answer to the P/E ratio, and it is the workhorse multiple in private equity and M&A.

Enterprise value (EV) is what it would cost to buy the entire business: its equity (market cap) plus the debt you would inherit, minus the cash you would get. Because EV includes debt, EV/EBITDA is a more complete valuation lens than the P/E ratio for comparing companies with different debt loads. A lower multiple generally signals a cheaper valuation, all else equal.

So what is a normal EV/EBITDA multiple? As of mid-2026, the global median deal multiple sat near 10.7x, the highest since 2021, with most industries clustering between 10x and 20x. But the range is enormous by sector:

| Sector | Typical EV/EBITDA (2026) | Why |

|---|---|---|

| System & application software | ~28x - 32x | High growth, high margins, asset-light |

| Technology & healthcare | ~12.5x - 12.8x | Strong growth and profitability |

| Broad market median | ~10.7x | The all-industry midpoint |

| Energy & materials | ~7.4x - 8.9x | Cyclical, capital-intensive, lower growth |

The takeaway: a 9x multiple is cheap for a software company and expensive for an oil producer. Always judge EV/EBITDA against a company's own sector and history. You can screen and rank stocks by valuation and quality metrics on the market screener, and dig into bargain candidates with our beginner's guide to deep value stocks. For cheaper, asset-heavy names, EV/EBITDA pairs well with the price-to-sales ratio.

Why Do Buffett and Munger Call EBITDA "Bullshit Earnings"?

No discussion of EBITDA is complete without the most famous critique in investing. At the 2003 Berkshire Hathaway annual meeting, Charlie Munger told shareholders: "Every time you see the word EBITDA, you should substitute the words 'bullshit earnings.'" He later described relying on it as "horror squared."

Warren Buffett's objection is more specific and, frankly, hard to argue with. His issue is with how EBITDA treats depreciation. As Buffett put it, "Does management think the tooth fairy pays for capital expenditures?" Depreciation, he argues, is a real expense - in fact "a cash expense. The only difference is that you spend it first." When you buy a machine, the cash leaves on day one; depreciation is just the accounting that spreads that cost across the years the machine is used. Adding it back, as EBITDA does, pretends a genuine cost never happened. You can read Munger's reasoning in this Yahoo Finance recap.

Their broader concern is cultural: when management fixates on EBITDA and "adjusted" earnings, it normalizes waving away real costs. Buffett has written that "a management that regularly attempts to wave away very real costs by highlighting adjusted per-share earnings makes us nervous." The critique is not that EBITDA is useless - it is that it is dangerous when treated as the bottom line rather than as one input among many.

Adjusted EBITDA: Helpful Tool or Red Flag?

If plain EBITDA already strips out four items, "adjusted EBITDA" goes further, removing additional costs management deems "one-time," "non-recurring," or "non-core" - things like restructuring charges, litigation costs, stock-based compensation, and acquisition expenses. Sometimes these adjustments are legitimate. Often they are a creative way to make a struggling business look profitable.

The legendary cautionary tale is WeWork, which in its 2019 IPO filing invented "Community-Adjusted EBITDA" - a figure that backed out not just interest, taxes, and depreciation, but also marketing, administrative, and development expenses. The result turned massive losses into a positive number. Investors saw through it, the IPO collapsed, and the term became a punchline for earnings manipulation.

How to keep yourself safe with adjusted EBITDA:

- Read the reconciliation. Public companies must reconcile adjusted EBITDA back to GAAP net income. Find that table and see exactly what was added back.

- Watch stock-based compensation. Adding back SBC is common in tech but controversial - it is a very real cost to shareholders through dilution.

- Be suspicious of "recurring non-recurring" items. If "one-time" charges appear every single quarter, they are not one-time.

- Compare the trend. If the gap between adjusted EBITDA and net income keeps widening, ask why.

How to Use EBITDA Without Getting Burned

EBITDA is a tool, and like any tool it is useful in the right job and dangerous in the wrong one. Here is a practical framework for using it well:

1. Use it to compare, not to value in isolation

EBITDA shines when you compare similar companies in the same sector. It is far less useful as a single verdict on whether a business is "good."

2. Always pair it with free cash flow

Before you trust an EBITDA number, calculate free cash flow. If EBITDA is high but free cash flow is thin, capital spending is eating the profits and EBITDA is overstating reality.

3. Subtract capex mentally

A quick sanity check is EBITDA minus capex (sometimes called EBITDA-capex or "owner earnings" in spirit). For a capital-intensive business, this can be dramatically lower than EBITDA alone.

4. Respect the debt EBITDA hides

EBITDA ignores interest, but debt does not ignore you. A company with strong EBITDA and crushing debt can still go bankrupt. Always check the debt load alongside the EBITDA. Our guide to analyzing a stock before buying covers the balance-sheet checks that go with this.

5. Let an AI assistant do the heavy lifting

You do not have to dig through filings by hand. You can ask the Finance Halo market intelligence dashboard or the AI chat to pull a company's EBITDA, margin, and EV/EBITDA, then compare them to peers in seconds.

Common Mistakes to Avoid

- Treating EBITDA as cash flow. It is not. It ignores capex, working capital changes, interest, and taxes - all of which consume real cash. Always confirm with free cash flow.

- Ignoring capital intensity. EBITDA flatters capex-heavy businesses (telecom, airlines, utilities) most, because it adds back their largest real cost.

- Comparing margins across industries. A 15% EBITDA margin is great for a grocer and weak for a software firm. Compare only within a sector.

- Trusting "adjusted EBITDA" blindly. Always read the GAAP reconciliation and scrutinize what management added back.

- Forgetting the debt. Strong EBITDA does not prevent bankruptcy when interest payments overwhelm cash flow. Check leverage.

- Using it alone. No single metric tells the whole story. Combine EBITDA with P/E, free cash flow, and the P/E, EPS, and PEG framework.

Frequently Asked Questions

What is EBITDA in simple terms?

EBITDA is a company's operating profit before subtracting interest, taxes, depreciation, and amortization. In plain English, it estimates how much cash the core business produces before financing and accounting choices are factored in.

How do you calculate EBITDA?

Two ways. Either start from net income and add back interest, taxes, depreciation, and amortization; or start from operating income (EBIT) and add back only depreciation and amortization. Both give the same result.

What is a good EBITDA margin?

It depends on the industry, but a margin above 10% is generally considered healthy. Margins of 20% to 40% signal strong operating efficiency, and above 40% is exceptional - typical of software, luxury, and semiconductor companies.

Is EBITDA the same as profit?

No. EBITDA is a measure of operating performance, not bottom-line profit. Net income is the true accounting profit shareholders keep, because it accounts for interest, taxes, and depreciation that EBITDA deliberately ignores.

Why do investors use EBITDA instead of net income?

Because it improves comparability. By removing financing and tax effects, EBITDA lets investors compare the core operations of companies with different debt levels, tax situations, and accounting policies on a more level basis.

What is a good EV/EBITDA ratio?

The broad-market median was around 10.7x in mid-2026. Below the sector average can signal a bargain, but software trades near 28x to 32x while energy trades near 7x to 9x, so always compare within the same industry.

Why does Warren Buffett dislike EBITDA?

Because it adds back depreciation, which Buffett considers a real cash expense - the money was simply spent earlier to buy the asset. He and Charlie Munger argue EBITDA flatters capital-intensive businesses and can mask real costs.

Where can I find a company's EBITDA?

You can calculate it from the income statement (operating income) and cash flow statement (depreciation and amortization) in a company's 10-K or 10-Q filing, or look it up directly on a financial platform like Finance Halo.

Conclusion

EBITDA - Earnings Before Interest, Taxes, Depreciation, and Amortization - is a powerful shortcut for comparing the core operating profitability of different companies, and the foundation of the EV/EBITDA multiple that dominates dealmaking. Calculated in two simple ways and summarized as an EBITDA margin, it strips away financing and accounting noise to reveal the engine of a business.

But remember the three things that matter most: EBITDA is not cash flow, it hides the real cost of capital spending and debt, and "adjusted" versions deserve healthy skepticism. Buffett and Munger's warning is not that you should never look at EBITDA - it is that you should never stop there. Pair it with free cash flow and net income, judge it against sector peers, and you turn a much-abused metric into a genuinely useful one.

Try it yourself: Analyze AAPL with Finance Halo's AI assistant to get instant EBITDA, margins, valuation multiples, and peer comparisons in seconds - just type a ticker and ask.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Always do your own research before making investment decisions.