SpaceX IPO: Is SPCX Worth $1.75 Trillion?

6/14/2026

On June 12, 2026, SpaceX became a public company in the largest IPO in history, listing on the Nasdaq as SPCX at $135 a share for a $1.75 trillion valuation. The question every investor is asking: is SpaceX actually worth that, or is the market pricing a rocket that has not launched yet?

The Largest IPO in History: What Happened on June 12

After years of speculation, SpaceX (SPCX) finally went public. The company filed its S-1 registration on May 20, 2026, launched its roadshow on June 4, and began trading on the Nasdaq on June 12 under the ticker SPCX. The deal priced at $135 per share, with SpaceX selling 555.6 million shares to raise approximately $75 billion. At that price the company carried a $1.75 trillion valuation - the largest initial public offering in stock market history by a wide margin.

To put the scale in perspective: a single offering produced more exit value than essentially every venture-backed IPO of the prior decade combined. On day one, SpaceX was worth more than Tesla (TSLA), and on a revenue basis it debuted at a valuation larger than Tesla and Meta (META) combined. Elon Musk's rocket company entered the public market as one of the ten most valuable companies on Earth.

That is the headline. The harder question is whether the price reflects the business as it exists today, or a future that still has to be built. To answer it, you have to separate three things: what SpaceX earns now, what it could plausibly earn over the next decade, and how much the market is charging you for that upside. This article walks through all three with a realistic but optimistic lens - because the bull case here is genuinely enormous, and so is the multiple.

SpaceX by the Numbers: Revenue, Subscribers, and Launches

Before the valuation debate, the facts. SpaceX is not a pre-revenue moonshot - it is a real, fast-growing, operationally dominant business. In 2025 the company generated roughly $18 billion in consolidated revenue, up about 43% from $13.1 billion in 2024. The catch: it still reported a GAAP net loss of about $4.9 billion, the cost of building satellites, ramping Starship, and acquiring spectrum.

Here is the snapshot that matters most:

| Metric | 2024 | 2025 | Trend |

|---|---|---|---|

| Total revenue | ~$13.1B | ~$18B | +43% YoY |

| Starlink revenue | $7.7B | $11.4B | +48% YoY |

| Starlink subscribers (year-end) | 4.6M | 9M | ~2x |

| Launches | ~138 | 170 | 6th straight record |

| GAAP net income | Loss | -$4.9B | Heavy reinvestment |

By the first quarter of 2026, Starlink had already crossed 10.3 million paid subscribers, a 105% year-over-year surge, and the launch business was running a Falcon 9 mission every three to five days. Those are not the numbers of a science project. They are the numbers of an infrastructure company growing into a near-monopoly position - which is exactly why the valuation argument is so heated. For a refresher on reading a company's fundamentals before you judge its price, see our guide on how to analyze a stock before buying.

How Do You Even Value a Company Like SpaceX?

Here is the uncomfortable starting point. SpaceX has no earnings to anchor a P/E ratio on - it lost money in 2025. So the market reaches for the next-best yardstick: the price-to-sales ratio. The formula is simple:

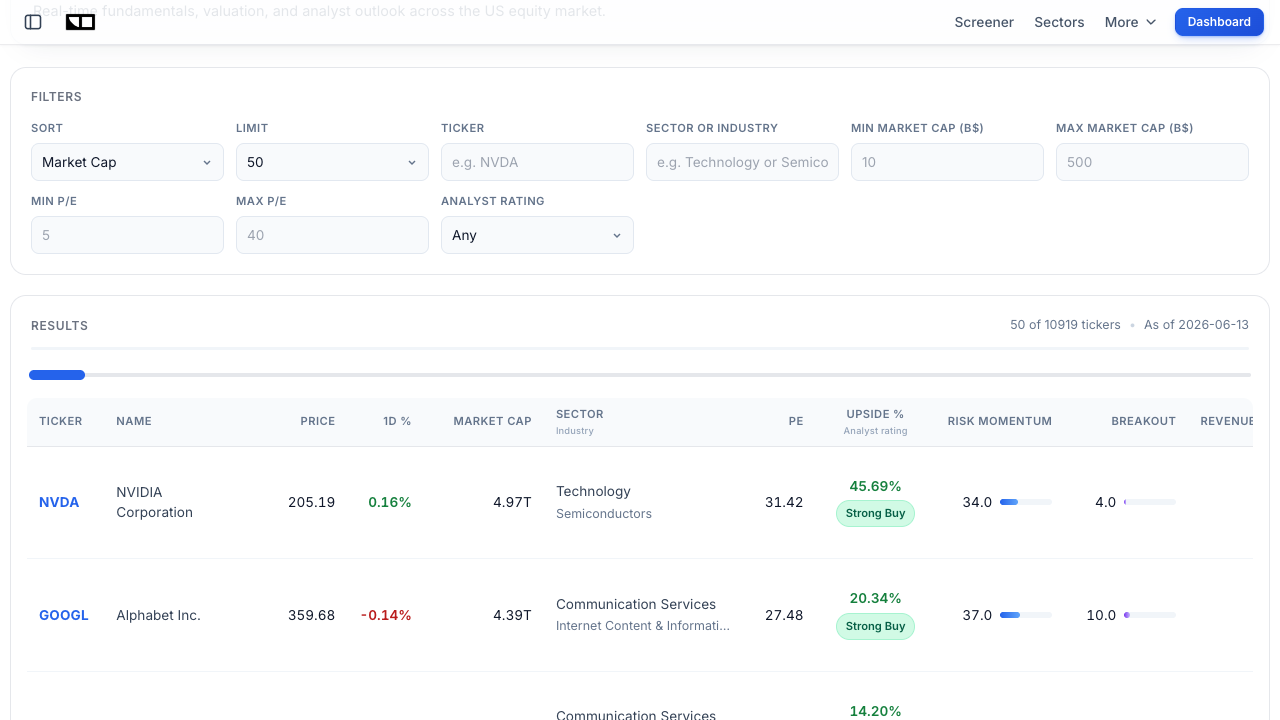

Run the math. A $1.75 trillion valuation on roughly $18 billion of trailing revenue works out to about 97 times sales. Different analysts use slightly different revenue and valuation figures, landing the multiple somewhere between 67x and 94x, but the conclusion is the same: this is one of the richest sales multiples ever applied to a company of this size. For context, NVIDIA (NVDA) - the poster child of the AI boom - trades around 23 times sales.

Why the P/S ratio is the right (and wrong) tool here

The price-to-sales ratio is the natural metric for a high-growth, low-or-negative-earnings company, which is why it suits SpaceX. But a 97x multiple only makes sense if you believe revenue will multiply many times over while margins expand. In other words, you are not paying for the $18 billion SpaceX earns today - you are paying for the $100 billion-plus the bulls think it could earn in the 2030s. If you want to understand what a sane sales multiple looks like across industries, our explainer on what is a good price-to-sales (P/S) ratio is the place to start.

Growth has to do the heavy lifting

The optimistic framing is that SpaceX is the rare company where a triple-digit sales multiple can be grown into. If revenue compounds at 35-45% for several years - entirely plausible given Starlink's trajectory - the multiple compresses on its own without the stock falling. The pessimistic framing is that any stumble in subscriber growth, launch cadence, or Starship economics removes the justification for the premium all at once. Both can be true. You can screen and compare valuation multiples for any public company using the Finance Halo market screener.

Starlink: The Cash Engine Behind the Valuation

If you only understand one thing about the SpaceX bull case, make it this: Starlink is the profit center, and it is compounding faster than almost any consumer subscription business in history. In 2025 Starlink produced $11.4 billion of revenue - 61% of the company total - up 48% year over year. More importantly, it threw off roughly $4.4 billion in operating profit, making it SpaceX's core earnings engine even while the consolidated company posted a loss.

The subscriber flywheel

Starlink subscriber growth has gone vertical. Look at the cadence:

| Date | Paid subscribers | Note |

|---|---|---|

| Year-end 2024 | 4.6 million | Base year |

| December 2025 | 9 million | Roughly doubled in 12 months |

| Q1 2026 | 10.3 million | +105% year over year |

| End-2026 (projected) | 16-18 million | $15.9-20B revenue range |

The reason this matters for valuation is operating leverage. The constellation is a fixed-cost asset: once the satellites are up and the ground stations are built, each new subscriber is largely incremental margin. As Starlink layers in higher-value enterprise, maritime, and aviation customers - who pay far more than a residential user - average revenue per user climbs while the satellite cost base stays roughly flat. That is the textbook recipe for margin expansion, and it is the single strongest pillar under the $1.75 trillion number.

From consumer broadband to global connectivity utility

Residential internet is just the entry point. Starlink is increasingly an enterprise and government connectivity utility: airlines wiring their fleets for in-flight Wi-Fi, shipping companies connecting vessels, telecoms backhauling rural towers, and militaries buying resilient comms. Each of these is a higher-margin, stickier revenue stream than a $120-a-month home subscription. The realistic optimist's view is that Starlink alone - if it reaches 40-50 million subscribers across these tiers by the early 2030s - could justify a large fraction of today's valuation on its own.

Launch Dominance: The Falcon 9 Moat

Starlink would not exist without the cheapest, most reliable launch system ever built. SpaceX flew 170 missions in 2025 (165 Falcon 9 and 5 Starship test flights), its sixth consecutive annual launch record, and now controls an estimated 82% of the global launch market - more flights than every other provider on the planet combined.

The moat is economic, not just operational. By reusing Falcon 9 first stages up to 29 times, SpaceX has cut the marginal cost of a launch to roughly $30 million, against $80 million for traditional expendable rockets - a cost advantage of about 70%. That lets the company do something no competitor can: launch its own Starlink satellites at internal cost while charging external customers a market price, effectively subsidizing its constellation with its launch monopoly.

- Cadence: a Falcon 9 launch every 3-5 days, 130+ missions a year.

- Reusability: boosters reused up to 29 times, slashing per-mission cost ~70%.

- Market share: ~82% of global launches, a near-monopoly position.

- Vertical integration: SpaceX is its own biggest launch customer via Starlink.

This vertical integration is the under-appreciated part of the story. SpaceX is simultaneously the lowest-cost producer in launch and the largest consumer of launch services - a closed loop that competitors like Amazon's (AMZN) Project Kuiper, which has to buy launches on the open market, simply cannot replicate.

Starship: The Trillion-Dollar Option Nobody Has Priced

If Falcon 9 is the engine of today, Starship is the call option on tomorrow. The fully reusable super-heavy vehicle is designed to drop launch costs by another order of magnitude and to lift the next generation of Starlink satellites - units SpaceX says will carry up to 100 times the capacity of the first generation.

Why does this matter for SPCX shareholders? Because cheaper, higher-capacity launch directly improves Starlink's unit economics - more bandwidth per satellite, fewer dollars per gigabit - while opening entirely new markets: heavy commercial payloads, lunar and Mars cargo, point-to-point Earth transport, and national-security missions that demand massive lift. None of these are in the current $18 billion revenue base.

The realistic caveat: Starship is still in its flight-test era, with only a handful of orbital attempts behind it. Operational, revenue-generating Starship service at scale is a multi-year project with real technical risk. The optimistic read is that the market is essentially getting this option for free if you believe the Starlink-plus-launch business already justifies most of the price. The bearish read is that a chunk of the $1.75 trillion is paying upfront for a vehicle that has not yet flown a paying customer to orbit. Both are defensible, and your view on Starship is, in practice, your view on the stock.

Direct-to-Cell: SpaceX's Move on the Mobile Industry

The most under-discussed growth vector is Direct-to-Cell - beaming connectivity straight to ordinary smartphones with no special hardware, eliminating dead zones anywhere with a clear view of the sky. In September 2025, SpaceX acquired roughly $17 billion of spectrum licenses from EchoStar (SATS), a clear signal it intends to compete directly in mobile telecommunications, not just rural broadband.

SpaceX now operates more than 600 Direct-to-Cell satellites, and it projects next-generation units will deliver up to 100 times the capacity of the current fleet. The total addressable market here is staggering: global mobile connectivity is a multi-trillion-dollar industry, and even a small slice of it - emergency messaging, rural voice and data, partnerships with national carriers - would be material against an $18 billion revenue base.

- The pitch: universal coverage, no new phone required, partnered with terrestrial carriers.

- The asset: $17B of EchoStar spectrum plus a 600+ satellite head start.

- The TAM: a piece of the multi-trillion-dollar global mobile market.

- The risk: regulatory, capacity, and competition from terrestrial 5G/6G.

This is the kind of optionality that makes the bull case coherent: SpaceX is not a one-product company. It is a launch monopoly funding a broadband near-monopoly that is now reaching into mobile - three enormous markets stacked on one cost-advantaged infrastructure.

Defense and Government: The Sticky, High-Margin Backlog

Underneath the consumer story sits a quieter, extremely durable business: launching for the Pentagon, NASA, and allied governments. SpaceX's Space segment - launch revenue from outside customers - generated about $4.1 billion in 2025, driven primarily by defense and NASA contracts. Growth there was slower (around 8%), but the quality is exceptional: multi-year, high-margin, and effectively recession-proof.

Government and defense demand has two attractive properties for a public-market investor. First, it is sticky - national-security launch providers are not swapped out casually, and SpaceX is often the only certified option with the required cadence. Second, it diversifies the revenue base away from consumer-cyclical Starlink subscriptions, giving the stock a floor of dependable cash flow. In a macro environment where investors are rotating toward defensive, contract-backed revenue, this segment is more valuable than its modest growth rate suggests. You can track how defense and aerospace are performing relative to other sectors on the Finance Halo market intelligence dashboard.

The $1.8 Trillion Space Economy: SpaceX's Total Addressable Market

Now zoom all the way out. The reason a triple-digit sales multiple is even debatable is the size of the prize. According to a joint World Economic Forum and McKinsey analysis, the global space economy is projected to expand from roughly $630 billion in 2023 to $1.8 trillion by 2035 - a compound growth rate near 9% a year, well above global GDP. Even McKinsey's conservative scenario lands the sector at about $1.4 trillion.

| Space economy segment | 2023 | 2035 (forecast) |

|---|---|---|

| "Backbone" (rockets, satellites, hardware, orbital services) | ~$330B | ~$755B |

| "Reach" (connectivity, navigation, downstream data/services) | ~$300B | ~$1,035B |

| Total space economy | ~$630B | ~$1.8T |

Here is why this framing is so favorable to SpaceX: the fastest-growing, largest segment is "Reach" - the connectivity and downstream-data layer projected to more than triple to over $1 trillion. That is precisely where Starlink and Direct-to-Cell play. SpaceX is not fighting for a sliver of a static market; it is the dominant operator in the highest-growth segment of an industry set to nearly triple. The realistic optimist's case for SPCX is essentially this: if SpaceX captures even 20-30% of the value pools it already leads, the revenue base in the 2030s could be many multiples of today's, and a 97x sales multiple on 2025 revenue starts to look like a reasonable multiple on 2032 revenue.

Is SPCX Worth $1.75 Trillion? The Bull and Bear Case

So, the headline question. The honest answer is that SpaceX is simultaneously one of the best businesses in the world and an expensive stock - and both halves of that sentence matter. Here is the balanced ledger:

| Bull case (the optimist) | Bear case (the realist) |

|---|---|

| Starlink subs compounding 100%+ with expanding margins | ~94-97x sales vs ~23x for NVIDIA; priced for perfection |

| 82% launch monopoly with a 70% cost advantage | GAAP net loss of $4.9B in 2025; no earnings anchor |

| Starship + Direct-to-Cell are unpriced $1T+ options | Morningstar fair value ~$780B - roughly 48% below IPO |

| Leads the highest-growth slice of a $1.8T market | Starship still in test phase; execution and timing risk |

| Sticky defense/NASA backlog provides a cash-flow floor | Key-man risk and governance tied to Elon Musk |

The cleanest way to hold both ideas at once: SpaceX may well grow into its valuation, but buying at $1.75 trillion gives you very little margin of safety. Morningstar's $780 billion fair-value estimate is not a claim that SpaceX is a bad company - it is a claim that the price already embeds a near-flawless decade of execution. If you believe in the mission and the moat, the realistic move is to size the position for the volatility that always follows a hyped mega-IPO, not to bet the portfolio on day-one perfection. To understand why a high multiple alone is not a sell signal, our breakdown of P/E vs EPS vs PEG is a useful companion - growth changes what "expensive" means.

Real-World Example: Pricing SPCX Against NVIDIA and Tesla

Numbers in isolation do not tell you much. Comparison does. Let's put SPCX next to two reference points investors already understand - the AI hardware leader and Musk's other mega-cap.

| Company | Approx. valuation | Price-to-sales | Profitable? |

|---|---|---|---|

| SpaceX (SPCX) | ~$1.75T | ~94-97x | No (GAAP loss) |

| NVIDIA (NVDA) | ~$5T | ~23x | Yes, highly |

| Tesla (TSLA) | < SpaceX on day one | Lower | Yes |

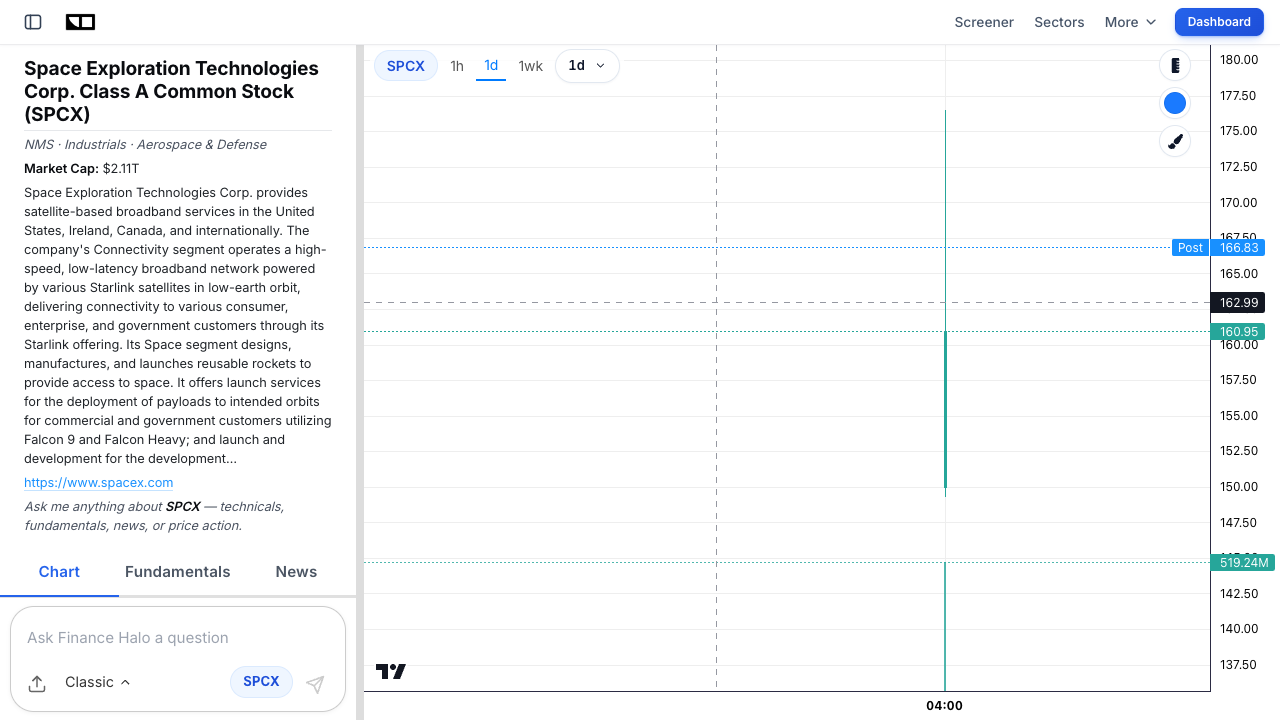

The takeaway is stark: investors are paying roughly four times NVIDIA's sales multiple for a company that, unlike NVIDIA, is not yet profitable. That does not make SPCX a bad investment - it makes it a bet on growth and TAM rather than on current earnings power. The mental model that fits SpaceX is closer to early Tesla or Amazon: years of reinvestment and losses while the platform scales, followed (if the bulls are right) by an inflection into enormous cash generation. You can pull up the live SPCX chart and ask the AI assistant about its valuation, technicals, and news directly.

One practical note on the chart above: because SPCX only began trading on June 12, the price history is just a few sessions long, and early post-IPO trading is notoriously volatile as the lock-up dynamics, index inclusion, and price discovery play out. Treat the first few weeks as noise, not signal.

Common Mistakes Investors Make With SPCX

- Confusing a great company with a great stock: SpaceX can be the best space company in history and still be a poor entry at 97x sales. Price and quality are separate questions - always.

- Anchoring on the IPO price: $135 is not a "fair value," it is a deal price set by bankers and demand. Morningstar's $780 billion estimate is a reminder that the float can re-rate hard in either direction.

- Buying into day-one euphoria: chasing a hyped mega-IPO on its first green candle is how investors end up underwater. Mega-IPOs frequently sell off after the initial pop and lock-up expirations.

- Ignoring the $4.9B loss: SpaceX is unprofitable on a GAAP basis. If you need earnings or free cash flow today, this is not your stock - the thesis is entirely forward-looking.

- Underestimating key-man and governance risk: the company is deeply tied to Elon Musk's vision and capital-allocation decisions. That is a feature in the bull case and a risk in the bear case.

- Position sizing like it is a blue chip: a newly public, story-driven mega-cap should be sized for 30-50% drawdowns, not treated like a stable dividend payer.

Frequently Asked Questions

Is SpaceX stock (SPCX) a good buy at $1.75 trillion?

It depends entirely on your time horizon and risk tolerance. The business is dominant and fast-growing, but at roughly 94-97 times sales the stock prices in years of flawless execution. Long-term believers may accumulate gradually; value-focused investors will likely find the margin of safety too thin at the IPO price, with Morningstar estimating fair value near $780 billion.

What ticker does SpaceX trade under?

SpaceX trades on the Nasdaq under the ticker SPCX. It began trading on June 12, 2026 at an IPO price of $135 per share.

How does SpaceX make money?

Most of SpaceX's revenue - about 61% in 2025 - comes from Starlink, its satellite broadband service. The rest comes from its launch business (Falcon 9 and Falcon Heavy missions for commercial, NASA, and Pentagon customers) and emerging segments like Direct-to-Cell mobile connectivity. Starlink is also the company's main profit center, generating roughly $4.4 billion of operating profit in 2025.

Why is SpaceX valued so much higher than its revenue?

Because investors are paying for future growth, not current sales. The bet is that Starlink subscribers, launch volume, Direct-to-Cell, and Starship will multiply SpaceX's revenue many times over by the 2030s as the broader space economy grows toward $1.8 trillion. The valuation reflects total addressable market and growth, not today's $18 billion in revenue.

Is SpaceX profitable?

Not on a consolidated GAAP basis - the company reported a net loss of about $4.9 billion in 2025 due to heavy reinvestment in satellites, Starship, and spectrum. However, the Starlink segment is profitable on its own, generating around $4.4 billion in operating profit, which is a key part of the bull case.

What are the biggest risks to the SPCX investment thesis?

The main risks are valuation (any growth stumble removes the justification for a 97x multiple), Starship execution and timing, regulatory hurdles in mobile and spectrum, key-man dependence on Elon Musk, and the typical post-IPO volatility and lock-up selling that hit newly public mega-caps. The business quality is high; the price is where the risk concentrates.

How big is SpaceX's total addressable market?

Very large. The global space economy is forecast to grow from roughly $630 billion in 2023 to $1.8 trillion by 2035, with the connectivity and downstream-data segment - where Starlink and Direct-to-Cell operate - growing fastest to over $1 trillion. SpaceX is the dominant player in the highest-growth slice of that market.

Should I wait before buying SPCX?

Many investors prefer to let a hyped mega-IPO settle before committing capital, since early trading is volatile and lock-up expirations can pressure the price months later. Dollar-cost averaging into a position over time, rather than buying all at once on day one, is a common way to manage that uncertainty - see our guide on dollar-cost averaging vs lump-sum investing.

Conclusion

So is SPCX worth $1.75 trillion? The realistic-but-optimistic answer is: the business may well be, in time - the stock demands you pay for that future today. SpaceX is a genuinely exceptional company: an 82% launch monopoly with a 70% cost advantage, a broadband service compounding past 10 million subscribers with expanding margins, an unpriced Starship-and-Direct-to-Cell option stack, and a sticky defense backlog - all aimed at the highest-growth segment of a $1.8 trillion market. That is the strongest TAM story in public markets right now.

But great businesses and great entry prices are different things. At roughly 94-97 times sales, with a $4.9 billion loss and Morningstar's fair value sitting nearly 48% below the IPO price, SPCX offers almost no margin of safety. The optimistic case is that growth grows the company into the multiple; the realistic case is that you should size the position for serious volatility and let price discovery do its work before backing up the truck. Believe in the mission, respect the math, and let valuation - not hype - guide your timing.

Try it yourself: Analyze SPCX with Finance Halo's AI assistant to get instant valuation context, technical analysis, and the latest news on SpaceX in seconds.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Always do your own research before making investment decisions.